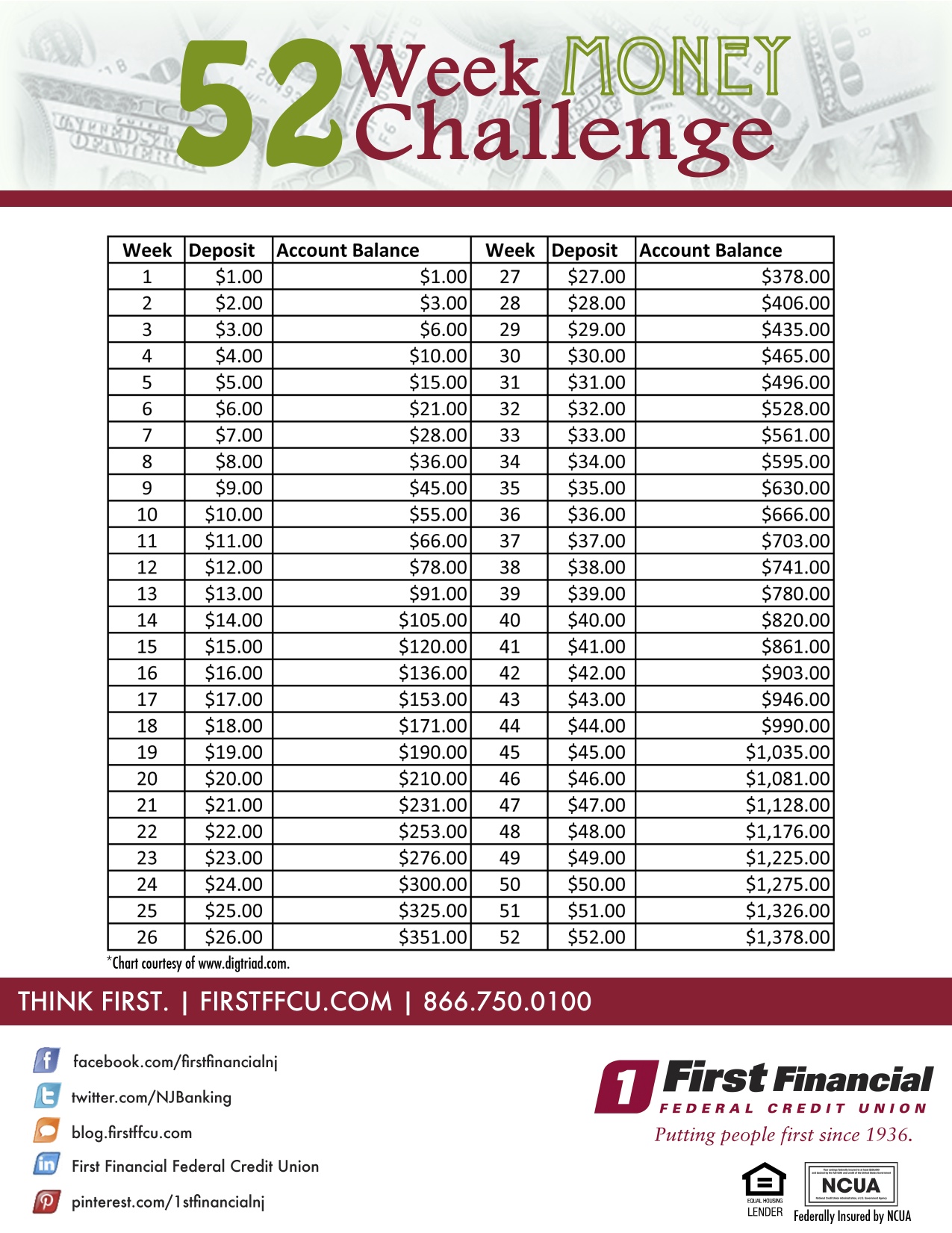

Start your new year off the right way – by saving money. Take the 52 week money challenge below, and you’re guaranteed to save almost $1,400 by the start of the new year. Ready, set, go!

Start your new year off the right way – by saving money. Take the 52 week money challenge below, and you’re guaranteed to save almost $1,400 by the start of the new year. Ready, set, go!

Public computers in libraries, Internet cafes, airports, and copy shops can be safe if you follow a few simple rules when you use them. Read these tips to help keep your work, personal, or financial information private.

Public computers in libraries, Internet cafes, airports, and copy shops can be safe if you follow a few simple rules when you use them. Read these tips to help keep your work, personal, or financial information private.

T.H.I.N.K First because There’s Harm In Not Knowing

For many families, using an allowance to encourage children to do chores is an effective means of both teaching responsibility and money management. For other families, linking chores to an allowance means that the children only learn to help out around the house in exchange for payment. It is important for parents to sit down and talk about what they hope their children learn from the experience of getting an allowance. Here are three common methods you may wish to consider implementing:

For many families, using an allowance to encourage children to do chores is an effective means of both teaching responsibility and money management. For other families, linking chores to an allowance means that the children only learn to help out around the house in exchange for payment. It is important for parents to sit down and talk about what they hope their children learn from the experience of getting an allowance. Here are three common methods you may wish to consider implementing:

The “You’re Part of the Family” Strategy

This strategy hinges on a few things: adult family members must always set a good example when it comes to their own chores, and the chores given to a child must bring them closer to the whole family. Family work days are effective ways of making this strategy work. The downfall of this strategy is that it can often be harder to track what, when and how well a child completes their given tasks.

The “Must Work for Your Pay” Technique

This technique links each separate job with an amount of pay. The benefit of this style is that it can make keeping track of completed tasks much easier. To make this work, very clear expectations must be set both with a timetable and in regards to how to correctly carry out each task. The downside is that since the children link a task to a certain amount of money, they may decide the amount is not worth the work required to complete the task. This can cause friction and frustration with parents and children.

The “Request as Needed” Method

This method involves you allowing your child to make requests to you for the things they want, which can allow you to help your child verbalize why what he or she wants, is important to them. It also builds their ability to negotiate and be persuasive. The downside of this method, however, is that you will constantly be having your child ask for and negotiate for what he or she wants.

Whatever method you use, there are some universal tips for every allowance strategy:

Learning to work with money is an important childhood milestone. Giving an allowance can be a positive event that brings the family together instead of creating arguments.

ATTENTION PARENTS: Please bring your children in to take full advantage of our First Step Kid’s Savings Account* – a unique product that was specifically designed for young people, with a focus on education and fun and it’s a great way to encourage your kids to save every penny! We also offer our Dollar’s for A’s Program** and our annual Summer Reading Contest which additional ways your children can earn money while having fun doing it – for more information, visit our website.

This article written by our friend, Marcia Hall of GoNannies.com.

*A $5 deposit in a base savings account is required for credit union membership prior to opening any account. Parent or guardian must bring both the child’s birth certificate and social security card when opening a First Step Kids Account at any branch location. Parent or guardian will be a joint owner and must also bring their identification. A First Financial membership available to anyone who lives, works, worships, volunteers or attends school in Monmouth or Ocean Counties.

**Available for First Financial members between 1st and 12th grades. Child must be present and a deposit to a First Step Kids Account is required to receive the Dollars for A’s incentive. Offer applies only to report cards for most recent school terms. Qualifying report cards must be submitted within 45 days from the date of issue. No back rewards available for prior semesters or marking periods. Letter grade “A” (or school district’s equivalent) or 90%+. Limit of $10 will be rewarded for A’s per each marking period, not to exceed $40 in Dollars for A’s deposited per school year or calendar year.

Want to buy for everyone on your holiday list, but don’t want to go broke while doing so? Here are some tips to keep your holidays fun yet affordable!

Want to buy for everyone on your holiday list, but don’t want to go broke while doing so? Here are some tips to keep your holidays fun yet affordable!

*Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker/dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. First Financial Federal Credit Union (FFFCU) and First Financial Investment & Retirement Center are not registered as a broker/dealer or investment advisor. Registered representatives of LPL offer products and services using First Financial Investment & Retirement Center, and may also be employees of FFFCU. These products and services are being offered through LPL or its affiliates, which are separate entities from and not affiliates of FFFCU or First Financial Investment & Retirement Center.

Securities and insurance offered through LPL or its affiliates are:

![]()

“Don’t believe everything you hear.” How many times have you heard this when you were a kid? Well, everyone grows up and it’s time to actually listen to that little old saying, especially when it comes to buying a vehicle. There are tons of common myths and misconceptions out there, but what is the truth behind these myths? Find out the true answers to some of the most common car buying myths right here:

“Don’t believe everything you hear.” How many times have you heard this when you were a kid? Well, everyone grows up and it’s time to actually listen to that little old saying, especially when it comes to buying a vehicle. There are tons of common myths and misconceptions out there, but what is the truth behind these myths? Find out the true answers to some of the most common car buying myths right here:

Myth #1 Auto dealers will always have the best loan rate & payment.

This isn’t always necessarily true. Credit unions and other financial institutions also offer competitive rates compared to dealerships. Those who are looking into buying a car should shop around and not only compare rates, but also compare restrictions, to find the best deal that fits their wants and needs.

Myth #2 Seeking multiple pre-approvals/loan offers will destroy your credit rating.

An individual’s credit score will not be affected negatively if seeking multiple offers. The analysis will have to be made within a certain time period of 14 days. However, keep in mind while shopping around this may cause multiple creditors to request a consumer’s credit report.

Myth #3 Auto loan refinancing is expensive.

It’s actually the opposite. Refinancing can drastically reduce your monthly payments and is an option you should consider. Have you stopped into your local First Financial branch location to see how much we may be able to save you each month by refinancing your car loan? Or give us a call at 732.312.1500, Option 4.

Myth #4 Refinancing isn’t an option on an auto loan.

Most people know that refinancing an auto loan can provide the same benefits as refinancing a home loan. They both can save you a lot of money by lowering the monthly payment or interest rate. Many may not know that refinancing an auto loan is actually much easier than refinancing a home loan. You might want to consider refinancing if your current car loan interest rate is above 6 percent, doing so could save you hundreds of dollars each year if you are approved!

Myth #5 Consumers think that even though Credit Unions have better rates – that you have to have perfect credit to get them, or be part of a union or work at a certain company to get them.

You do have to be a member of a Credit Union to get the Credit Union’s rates, and the rate you qualify for is based on your credit worthiness. However, most people do not realize just how easy it is to join a Credit Union these days, and that Credit Unions will at least try to work with you and help you get on the right track to a better financial standing if you aren’t currently. The majority of Credit Unions how have community charters – where you simply need to live, work, worship, or attend school in a certain area in order to become a member of that particular Credit Union. That’s certainly the case at First Financial – to join $5 in a Base Savings Account is needed at all times, and you must live, work, worship, volunteer, or attend school in Monmouth or Ocean Counties in New Jersey. Plus, once you are a member – your immediate family can join too.

As always, First Financial offers great low rates – and they’re the same whether you plan to purchase a new or used vehicle!

In the frenzy of limited time offers, last minute sales and one-click shopping, it can be difficult to stay secure while you shop online, particularly on days like Cyber Monday.

In the frenzy of limited time offers, last minute sales and one-click shopping, it can be difficult to stay secure while you shop online, particularly on days like Cyber Monday.

Consumers spend about 1.5 billion dollars on Cyber Monday. Coupled with the boom in sales is a predicted increase in the amount and severity of online scamming and data theft.

Will Pelgrin, CEO of The Center for Internet Security (CIS), a non-profit organization focused on improving the cyber-security posture of both the private and public sector, shares a few helpful tips about staying secure online this season.

Though it may seem obvious, malicious pop-up ads still pose one of the largest threats to web shoppers. According to Pelgrin, studies have shown that a large amount of consumers will click on the “ad” regardless of its message. Be mindful of what pop-ups say, it could be evidence of a security threat.

Though many systems automatically update your software as new features become available, it’s important to keep your programs as current as possible. To avoid security holes, update apps and software minimally once a week, as newer versions appear.

An essential part of online security in any sense is using strong passwords. This means no birthdays, dog names or variations of “1234” for any of your accounts. For help making a strong password, check out this guide: How to Create a Secure Password.

When shopping, you don’t want others to be able to track what sites you’re visiting and what information you’re entering online. It’s important to make sure you have antivirus software installed on your computer to protect your sensitive financial information.

According to Pelgrin, more and more consumers are doing the bulk of their holiday shopping on mobile phones. If you’re one of those consumers, make sure to enable a lock screen password, in case your device is lost or stolen. “If your phone isn’t timed out, you’re leaving the keys to your kingdom to whoever picks it up,” says Pelgrin.

Pelgrin recommends that any and all online financial transactions take place through a secure, private Wi-Fi connection, as opposed to using the more vulnerable free Wi-Fi in a coffee shop or library.

Your inbox is likely swarming with holiday promotions from all of your favorite (and likely least favorite) brands. To avoid being hacked, the CIS recommends you always enter the shop’s URL in your browser, rather than following the links contained in an email.

Before you buy from a merchant on Amazon, Etsy or Ebay, check their rating and number of sales. Make sure they have good return policies and clearly posted contact information. If worried, you can always check on a businesses legitimacy through the Better Business Bureau.

“There are more security protections on your credit card that may not exist while using your debit card, should your info be taken,” says Pelgrin.

If you are entering your financial information on a webpage, make sure the URL begins with “https” as opposed to “http” or has a lock in your browser’s search bar.

Though the holidays are frequently the most popular time to make donations to charity, Pelgrin urges consumers to check the legitimacy of your charity’s website.

“Fraudulent sites pop up during disasters and holidays like clockwork. Be alert,” he says.

Many apps and websites will automatically share your GPS location by default. Sometimes, apps will change your settings once downloaded. Check what services your downloads have access to in your phone’s privacy settings.

According to Pelgrin, some hackers will do very low level theft once obtaining your information, charging small amounts to your credit card to avoid detection. Stay on top of your account statements and keep a record of how much you spend and where.

Pop-up blockers and malware detection extensions will add an extra layer to your security this season.

Happy Safe Shopping!

Click here to view the article source by Max Knoblauch of Mashable.